This topic recorded the taxes and mandatory contributions that a medium-size company must have paid or withheld in a given year, as well as the administrative burden of paying taxes and contributions. The most recent round of data collection for the project was completed on May 1, 2019 covering for the Paying Taxes indicator calendar year 2018 (January 1, 2018 – December 31, 2018). See the methodology and video for more information.

To learn more about the results of Paying Taxes in calendar year 2018, see the Paying Taxes 2020 report.

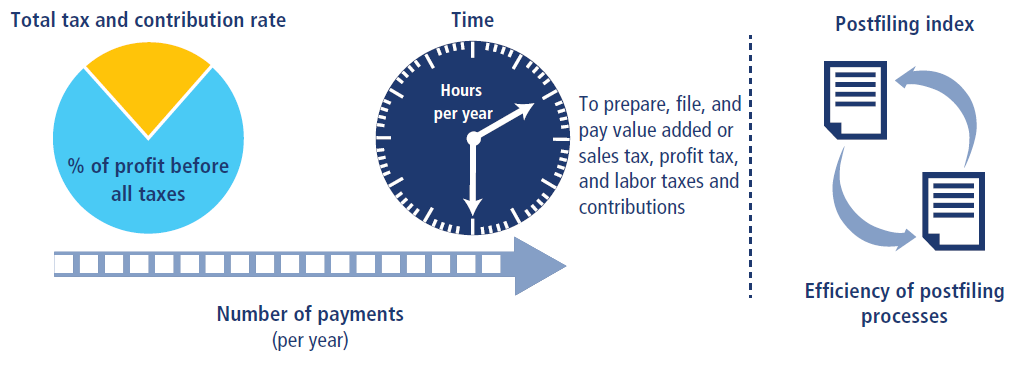

Doing Business records the taxes and mandatory contributions that a medium- size company must pay in a given year as well as measures of the administrative burden of paying taxes and contributions and complying with postfiling procedures. The project was developed and implemented in cooperation with PwC. Taxes and contributions measured include the profit or corporate income tax, social contributions and labor taxes paid by the employer, property taxes, property transfer taxes, dividend tax, capital gains tax, financial transactions tax, waste collection taxes, vehicle and road taxes, and any other small taxes or fees.

Source: Doing Business database

The ranking of economies on the ease of paying taxes is determined by sorting their scores for paying taxes. These scores are the simple average of the scores for each of the component indicators, with a threshold and a nonlinear transformation applied to one of the component indicators, the total tax and contribution rate. The threshold is defined as the total tax and contribution rate at the 15th percentile of the overall distribution for all years included in the analysis up to and including Doing Business 2015, which is 26.1%. All economies with a total tax and contribution rate below this threshold receive the same score as the economy at the threshold.

The threshold is not based on any economic theory of an “optimal tax rate” that minimizes distortions or maximizes efficiency in an economy’s overall tax system. Instead, it is mainly empirical in nature, set at the lower end of the distribution of tax rates levied on medium-size enterprises in the manufacturing sector as observed through the paying taxes indicators. This reduces the bias in the total tax and contribution rate indicator toward economies that do not need to levy significant taxes on companies like the Doing Business standardized case study company because they raise public revenue in other ways—for example, through taxes on foreign companies, through taxes on sectors other than manufacturing or from natural resources (all of which are outside the scope of the methodology).

Doing Business measures all taxes and contributions that are government mandated (at any level—federal, state or local) and that apply to the standardized business and have an impact in its financial statements. In doing so, Doing Business goes beyond the traditional definition of a tax. As defined for the purposes of government national accounts, taxes include only compulsory, unrequited payments to general government. Doing Business departs from this definition because it measures imposed charges that affect business accounts, not government accounts. One main difference relates to labor contributions. The Doing Business measure includes government-mandated contributions paid by the employer to a requited private pension fund or workers’ insurance fund. It includes, for example, Australia’s compulsory superannuation guarantee and workers’ compensation insurance. For the purpose of calculating the total tax and contribution rate (defined below), only taxes borne are included. For example, value added taxes (VAT) are generally excluded (provided that they are not irrecoverable) because they do not affect the accounting profits of the business—that is, they are not reflected in the income statement. They are, however, included for the purpose of the compliance measures (time and payments), as they add to the burden of complying with the tax system.

Doing Business uses a case scenario to measure the taxes and contributions paid by a standardized business and the complexity of an economy’s tax compliance system. This case scenario uses a set of financial statements and assumptions about the transactions made over the course of the year. In each economy tax experts from a number of different firms (in many economies these include PwC) compute the taxes and mandatory contributions due in their jurisdiction based on the standardized case study facts. Information is also compiled on the frequency of filing and payments, the time taken to comply with tax laws in an economy, the time taken to request and process a VAT refund claim and the time taken to comply with and complete a corporate income tax correction.