This topic recorded the taxes and mandatory contributions that a medium-size company must have paid or withheld in a given year, as well as the administrative burden of paying taxes and contributions. The most recent round of data collection for the project was completed on May 1, 2019 covering for the Paying Taxes indicator calendar year 2018 (January 1, 2018 – December 31, 2018). See the methodology and video for more information.

To learn more about the results of Paying Taxes in calendar year 2018, see the Paying Taxes 2020 report.

Properly developed, effective taxation systems are crucial for a well-functioning society. In most economies, taxes are the main source of revenue to fund public spending on education, health care, public transport, infrastructure and social programs, among others. Tax policy is one of the most contentious areas of public policy. A large body of theoretical and empirical work examines the effects of high tax rates and complex fiscal systems. Although determining the optimal tax system can be challenging because context matters when economies want to maximize their welfare, there is less uncertainty—from both theoretical and empirical perspectives—about the distortionary effects of high taxes and cumbersome tax systems. A good tax system should ensure that taxes are proportionate and certain (not arbitrary) and that the method of paying taxes is convenient for taxpayers. Lastly, taxes should be easy to administer and collect.

Governments globally continue to do more to unlock the potential of technology to facilitate tax compliance. The data in Paying Taxes show how improvements in tax software, real time reporting systems and data analytics are easing the tax compliance on businesses. Even some advanced economies have continued to improve their tax administrations to the benefit of both taxpayers and tax authorities. New technology can drive considerable efficiencies for tax authorities and businesses alike. It is also important to consider that improvements to tax systems do not come from technology alone. Simple, coherent, well understood and properly administered tax systems are crucial to lower the barriers for businesses when complying with their tax obligations.

Côte D’Ivoire made the greatest advances in tax payment systems in calendar year 2018. The tax authority in Côte d'Ivoire fully implemented in 2018 an online payment system and a mobile payment for corporate income tax, value added tax, payroll taxes and other relevant taxes. The electronic filing system was already fully operational in 2017. Additionally, in 2018, the tax authority improved and expanded its online case management system for processing VAT cash refunds to cover all requests. The processing of the request for a VAT cash refund is carried out online and taxpayers can also follow up on their request electronically at the webpage of the tax authority. This has allowed the tax authority to be more efficient in refunding the VAT credits.

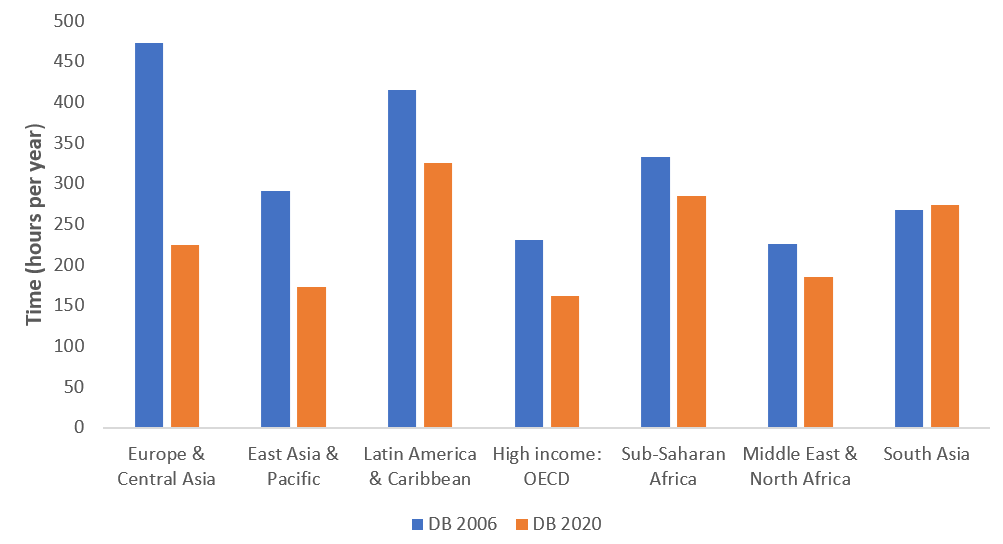

For the ninth year in a row, the most common feature of reforms in the area of paying taxes over the past year was the implementation or enhancement of electronic filing and payment systems. Seventeen economies—The Bahamas, Bahrain, China, Cote D’Ivoire, Cyprus, The Arab Republic of Egypt, Hungary, Indonesia, Israel, Jordan, Kenya, The Republic of Korea, Kyrgyz Republic, Pakistan, Russian Federation, Senegal and Vietnam—introduced or enhanced systems for filing and paying taxes online in 2018. The most notable progress since Doing Business 2006 in digitization has been the economies of Europe and Central Asia (figure 1). However, economies in the Sub-Saharan Africa region have been converging towards the good practice of moving from manual to online tax compliance systems.

Source: Doing Business database. Note: in South Asia, time in DB2020 is higher than time in DB2006 because of Maldives which in Doing Business 2013 have introduced the three major taxes: business profit tax, VAT and pension contributions. Therefore, compliance time in Maldives went up from 0 to 391 hours.

In Europe and Central Asia, 15 years ago the average compliance time was 473 hours per year. Thanks to the use of electronic systems for filing and paying taxes, economies in this region spent on average 225 hours on tax compliance in 2018. Sub-Saharan Africa remains the region with the smallest share of economies using electronic filing or payments. However, in 2018 the use of online systems for filing and payment of taxes resulted in efficiency gains in several economies in the region, including Côte d'Ivoire, Kenya, Mauritius and Senegal. The OECD high-income group has the highest prevalence of electronic systems, with 97% of economies having adopted them. As the costs of technology have fallen, more companies are using tax software and more tax authorities are creating easier-to-use online portals to simplify compliance.

Other economies directed their reform efforts at reducing the financial burden of taxes on businesses and keeping tax rates at a reasonable level to encourage private sector development. Nine economies have lowered their profit tax rates in 2018. The US Tax reform decreased corporate income tax rate from 34% to 21%. The new law also repealed the corporate alternative minimum tax. Morocco replaced the 30% flat corporate income tax rate with a progressive tax scale as of January 1, 2018.